One in three ships transporting Swedish goods that transits the Suez Canal carries forest products. Houthi rebel attacks on merchant ships in the Red Sea are deterring traffic through the canal, resulting in supply chain uncertainty and increased costs.

Sweden is one of the world’s largest producers of pulp, paper and sawn wood products. Eighty per cent of Swedish forest industry products are sold to other countries. This means that the sector provides climate benefits all over the world, but that it is also dependent on resilient logistics.

“We calculate that our industry is the single largest transport buyer of container freight from Sweden via the Suez Canal, where costs have now unexpectedly jumped by 100 to 200 per cent, so we view the future with some concern. There is a risk of container shortages, delays and disruption. Going around the Cape of Good Hope instead of via the [Suez] Canal can take up to 30 extra days for a round trip,” says Christian Nielsen, Market Expert Wood Products at Swedish Forest Industries.

“The current situation may continue for some time and result in cost increases, but above all increased uncertainty for the industry and for forest industry customers. However, since the autumn, there has been overcapacity of containers and vessels. Until now, shipping rates from Europe to Asia have been unusually low, which reduces near-term risk and helps calm the situation somewhat,” Nielsen says.

How are Swedish producers affected?

“In many cases, suppliers, especially of wood products, have managed to agree to share the increased costs with their customers. But of course they are affected. We’re already facing deteriorating economic conditions with falling prices, while production costs remain generally high. Margins are under more pressure than normal, which can have a severe impact on individual deliveries during this period. But over time, for new contracts, we believe that in many cases these are costs that customers in Asia will have to bear,” says Nielsen.

There are few alternatives to sawnwood imports from Europe, which appears to affect finished product prices in the region. The outlook is less certain for pulp and paper in terms of the impacts of cost increases and longer delivery times. Competition from other global suppliers is fiercer in these segments.

“This doesn’t necessarily mean that Swedish pulp producers will be hit harder than wood product producers. Competition is tougher in pulp and paper markets, but disruption to shipping will also affect imports of paper to Europe from low-cost producers in Asia. This could potentially increase demand in Europe.”

Will this also result in increased costs for wood products, pulp and cardboard on the Swedish market?

“No, I don’t think so. It’ll mainly affect our customers in Asia,” Nielsen says.

Facts

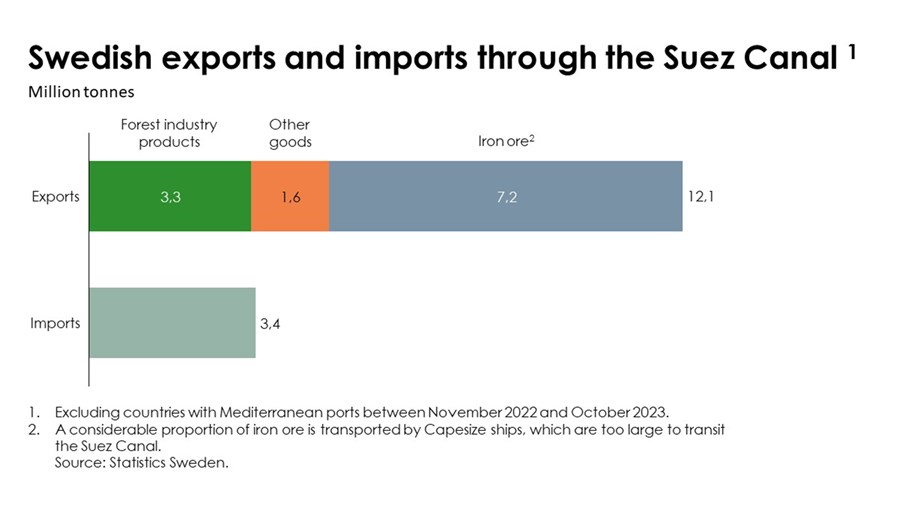

Of Sweden’s total forest industry exports, approximately 10 – 15 per cent were previously shipped via the Suez Canal and the Red Sea to customers in the Middle East and Asia. One third of Swedish exports (by volume) shipped via the Suez Canal are forest industry products. This is almost as much as Sweden’s total imports that transit the canal.